By Chris Whalen, C.P.A.

The House-Senate conference committee has issued their final version of the Trump Tax Plan. As I expected, this became law when it came to a vote before Christmas.

Remember, this is NOT retroactive to 1/1/2017, so your 2017 income tax returns will NOT be impacted.

I have been reviewing the entire bill since it became available. I believe most taxpayers will receive some tax benefits with this new law, but tax planning becomes more important than ever to make sure you are minimizing your tax liabilities within these substantial tax code changes.

Here are some highlights:

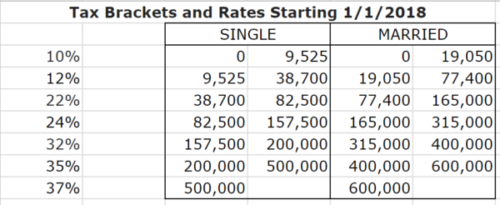

Income tax rates. We currently have seven (7) tax brackets: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. See the chart below for the new rates.

Pass-Through Entities. The owners of businesses filing as Sole Proprietorships, S Corps, Partnerships, LLC could see some tax savings. But these new rules are extremely complex and each situation needs to be analyzed individually. I urge you to schedule an appointment with me so I can review your current company’s structure, and see if the new law can benefit you.

The State and Local Income Tax Deduction is NOT repealed, but it might be limited for certain taxpayers. Under current law, the state and local deduction (SALT) is unlimited. Under the new law taxpayers will be able to deduct a COMBINED maximum of $10,000 in State and Local Income AND Property taxes. Preserving the state income tax deduction is great for middle class families. The law specifically states that you CANNOT prepay your state and local income taxes to avoid the cap BUT you can prepay the first 2 quarters of your 2018 real estate taxes.

Example: A married couple has $6,700.00 in property taxes and $4,000.00 in state income taxes paid. They will be able to deduct $10,000.00 maximum on their return. This is a good thing, as the deduction of state income taxes paid was almost eliminated.

The Alimony Deduction is eliminated for divorces settled AFTER 12/31/2018. This is NOT retroactive so any currently alimony arrangements still retain the tax deduction for the alimony payer, and the obligation to reflect alimony as income for the receiver.

Child Tax Credit, increases to $2,000 per child for families making up to about $400,000, but only $1,400 is refundable.

Obamacare Individual Mandate. Penalty eliminated for not having healthcare starting 2019.

Estate Tax Threshold increases to (single) $11 Million from $5.5 Million – to (married) $22 Million from $11 Million

Capital gains rates. Short term capital gains, (sales within one year of purchased) are taxed at your ordinary income tax rate. Long term capital gains are taxes at up to 20%.

Standard Deduction. The standard deduction amounts now increase to $12,000 for individuals, $18,000 for HOH, and $24,000 for married couples filing jointly.

Additional Standard Deduction & Personal Exemptions. ARE ELIMINATED. They were a $4,050 personal exemption for yourself, your spouse, and each of your dependents. This takes away most, if not all, of the benefit of the higher standard deductions mentioned above.

Mortgage Interest Deduction. New mortgages would be capped at $750,000 for purposes of the home mortgage interest deduction. Existing mortgage interest can still be taken up to the old limit of $1,000,000. Home Equity Debt Interest (meaning re-fis not related to improving your home) will be eliminated beginning in 2018.

Charitable Donation Deduction. Remains basically the same.

Medical Expense Deduction. Remains in place but with a LOWER floor 7.5% for tax years 2017 and 2018. This is a great change.

Miscellaneous Itemized Deductions. These are eliminated. These include Tax Preparation Expenses, Home Office Expenses and Unreimbursed Employee Expenses. That last one, Unreimbursed Employee Expenses, I covered in a separate blog post. Please read that immediately if you currently are an employee who takes these deductions. Click this link. Tax Memo – Have “Unreimbursed Business Expenses?”, Ask For A Raise Immediately

Above The Line Deductions. These are retained: student loan interest, tuition and fees, moving expenses and out-of-pocket teacher expenses.

American Opportunity Credit (AOC) and Lifetime Learning Credit (LLC). No Change.

Tuition Waivers For Graduate Students. Remain in place.

Fringe Benefits. Dependent Care and Adoption assistance remain in place, but the Moving Reimbursements as fringe benefits are eliminated, except for the Military.

529 Plans. Remains in place but with MORE flexibility. Now up to $10,000 per student can be used annually for private, public and religious elementary and secondary schools as well as home schooling.

Credit For The Elderly & Permanent Disabled. Remains in place.

Exclusion Of Gain From Sale Of Your Home. No change.

Alternative Minimum Tax (AMT). Still in place for individuals, but exemptions are increased which means few taxpayers will pay it.

Corporate Tax Relief. The Federal C Corporate Tax Rate is reduced to 21%

Please reach out to me without hesitation with any tax, business or accounting question, and to schedule a consultation.

Tax Laws are complex.

It is very easy to make mistakes that can incur penalties.

Do you have a Tax, Accounting or Business Question?

Call Me at (732) 673-0510. https://www.chriswhalencpa.com/